Financial Stability Report, December 2021

Systemic risk in the Polish financial system has declined, with legal risk of FX mortgage loans remaining the main risk

Od publikacji ostatniej edycji Raportu obniżyło się natężenie dotychczasowych źródeł ryzyka i poprawiła się ogólna ocena stabilności krajowego systemu finansowego.

Kapitały sektora bankowego tworzą wystarczający bufor na wypadek wystąpienia nieoczekiwanych szoków. Pomimo odbudowy zysków w 2021 r. niska rentowność sektora bankowego pozostaje wyzwaniem, szczególnie dla mniejszych banków, ale nie tworzy zagrożeń dla stabilności systemu. Również negatywne scenariusze rozwoju sytuacji w słabszych bankach nie zagrażałyby stabilności pozostałych podmiotów.

Ryzyko prawne mieszkaniowych kredytów walutowych pozostaje głównym źródłem ryzyka w systemie, jednak prawdopodobieństwo najbardziej kosztownych dla banków scenariuszy zmniejszyło się. Istotnie wrosły rezerwy na ryzyko prawne, jednak utrzymuje się ich silne zróżnicowanie pomiędzy bankami, co może budzić wątpliwości dotyczące adekwatnego odzwierciedlenie ryzyka w niektórych instytucjach.

Spodziewana jest dalsza odbudowa akcji kredytowej w głównych segmentach. Zagrożenie z tytułu niezrównoważonego wzrostu zadłużenia na rynku nieruchomości mieszkaniowych pozostaje ograniczone, choć przyspieszenie akcji kredytowej w tym segmencie wymaga ścisłego monitorowania.

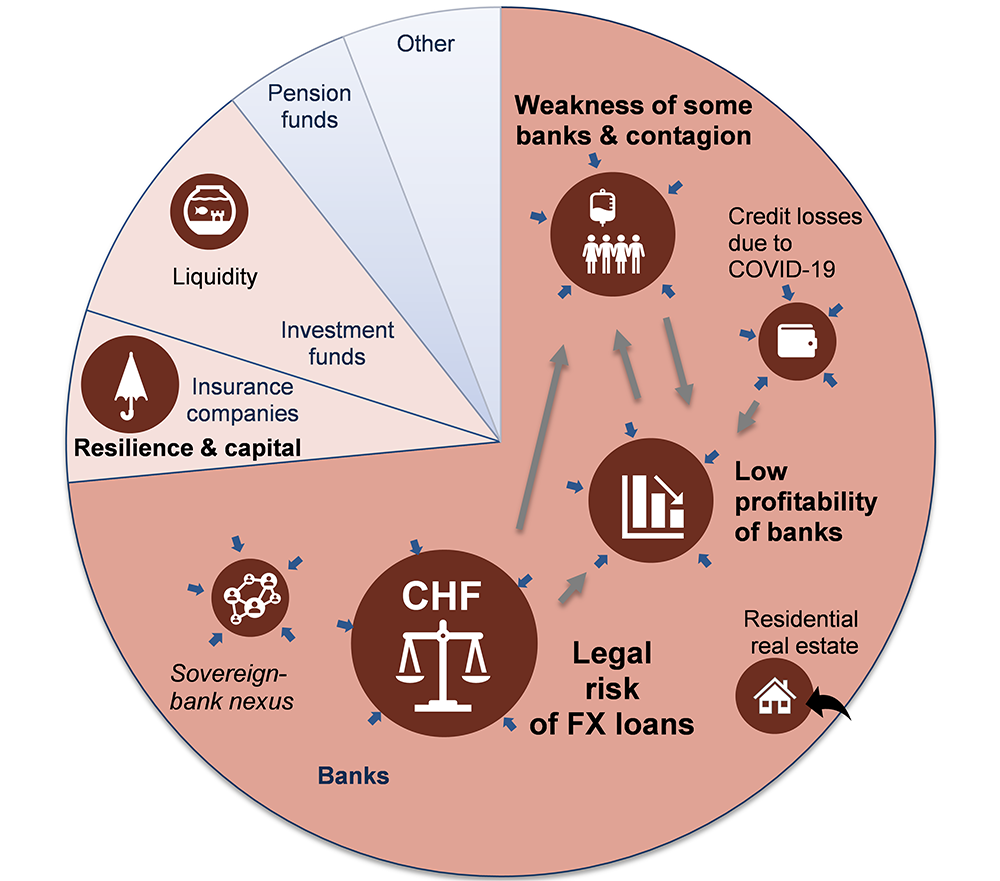

Notes: Shares of individual sectors (banks, insurance companies, etc.) reflect the value of their assets as at the end of 2020. The size of the circle describing the risk depends on the scale of risk (low, average, high). The main interactions – amplifications – across the risks are marked with grey arrows. Blue arrows pointing inwards particular risk denote a decrease in risk, while red arrows pointing outwards from the risk denote an increase in risk. A new risk is marked with a black arrow that goes from outside the circle. The colour of individual sectors shows systemic risk intensity – from very low risk (blue colour), through low and moderate to high (burgundy).

According to the opinion of Narodowy Bank Polski, the implementation of the following recommendations will be conducive to maintaining the stability of the domestic financial system.

- Banks, in cooperation with audit firms, should analyse whether their approach to creating provisions for legal risk associated with the FX housing loans portfolio is adequate.

- Banks and borrowers should seek more actively to settle their disputes out of court and reach settlements in FX housing loan cases.

- Banks should conduct a prudent lending policy with regard to the purchase of real estate and refrain from concentrating lending growth in this segment.

- It is advisable to speed up the process of integrating and merging cooperative banks to improve efficiency of the operating efficiency of the cooperative banking.

- Insurance companies should consider in their capital needs the issue of double gearing of capital and the high share of expected profits included in future premiums in own funds.

- Life insurance companies should refrain from offering unit-linked insurance policies which do not fulfil the basic cover component.

- Investment funds should reduce the scale of liquidity transformation and investment fund management companies should increase capital to provide support in the event of liquidity risk materializing in the funds they manage.